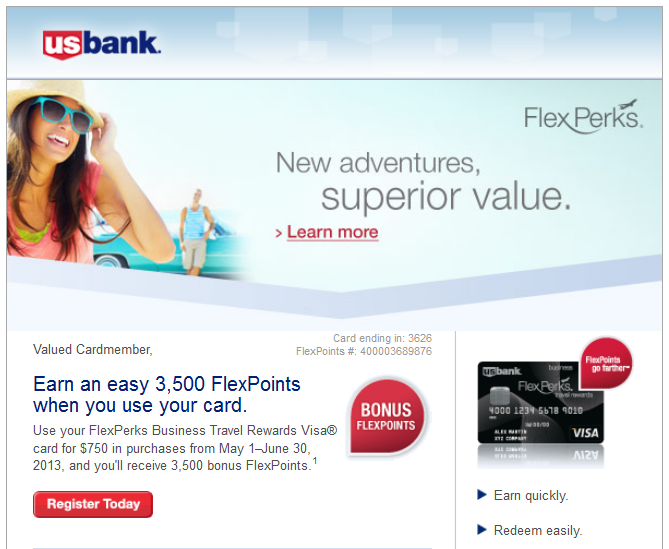

Targeted 3,500 U.S. Bank FlexPerks Offers

Yesterday I received in my email a targeted offer from my U.S. Bank FlexPerks cards (I have a personal and business version of the card), offering to award me 3,500 FlexPoints if I spend $750 between May 1 and June 30, 2013. After using both of our cards quite extensively in Hawaii last summer, once…